Each year, we create a data-backed map of where solar delivers the most value — highlighting the states with the strongest incentives and highest returns for commercial real estate owners and investors. We are excited to share the June 2025 “50 States of SolarKal” map!

This edition focuses on the states where there are exceptional opportunities to grow commercial solar and turn your portfolio’s solar potential into solar revenue. Understanding and tracking state solar policy is imperative to making commercial solar projects work for our clients, especially while there are changes to the federal policy being discussed.

Our current map reflects solar policies that have already passed, as well as key state and federal bills that may be finalized in June or July 2025. This year’s grading not only hinges on the evolution of solar credits in the federal landscape, but it also focuses on state-by-state incentives, utility electricity rates, net metering rules, and recent bills that support or discourage solar investments. For a deeper dive into how SolarKal grades each state, please read our blog post: An Inside Look at How SolarKal Grades Each State.

Our grading system evaluation focuses on key levers such as:

● State-level solar rebates and grants

● SREC (solar renewable energy certificates) markets and credit trading viability

● Net metering compensation and caps

● Community solar program stability

● Property tax and sales tax exemptions

● Permitting timelines and interconnection predictability

Maryland is stepping into the spotlight with the formal launch of its permanent community solar program. With the pilot sunset now behind, developers finally have a policy they can underwrite. Property tax exemptions remain in place, the SREC market is active, and projects up to 5 MW are now eligible under consistent program rules. With policy clarity and permitting streamlining underway, Maryland is becoming one of the most developer-friendly states on the East Coast.

Massachusetts has a new SMART program that we should look out for! The state is preparing to launch a next-generation solar incentive program, commonly referred to as SMART 2.0. If finalized as proposed, it could create some of the most favorable conditions for commercial solar in the U.S. — including some of the highest roof-lease rates in the country.

Rhode Island has promising grants available for small-scale commercial and community solar, making the state’s incentives more lucrative. Some of the standouts for us are the Renewable Energy Fund commercial grant program and the Renewable Energy Growth Program, offering incentives up to $75,000 along with a feed-in tariff program with an evolving virtual net metering structure. Rhode Island is also actively redesigning its community solar model to balance C&I offtake and equity targets.

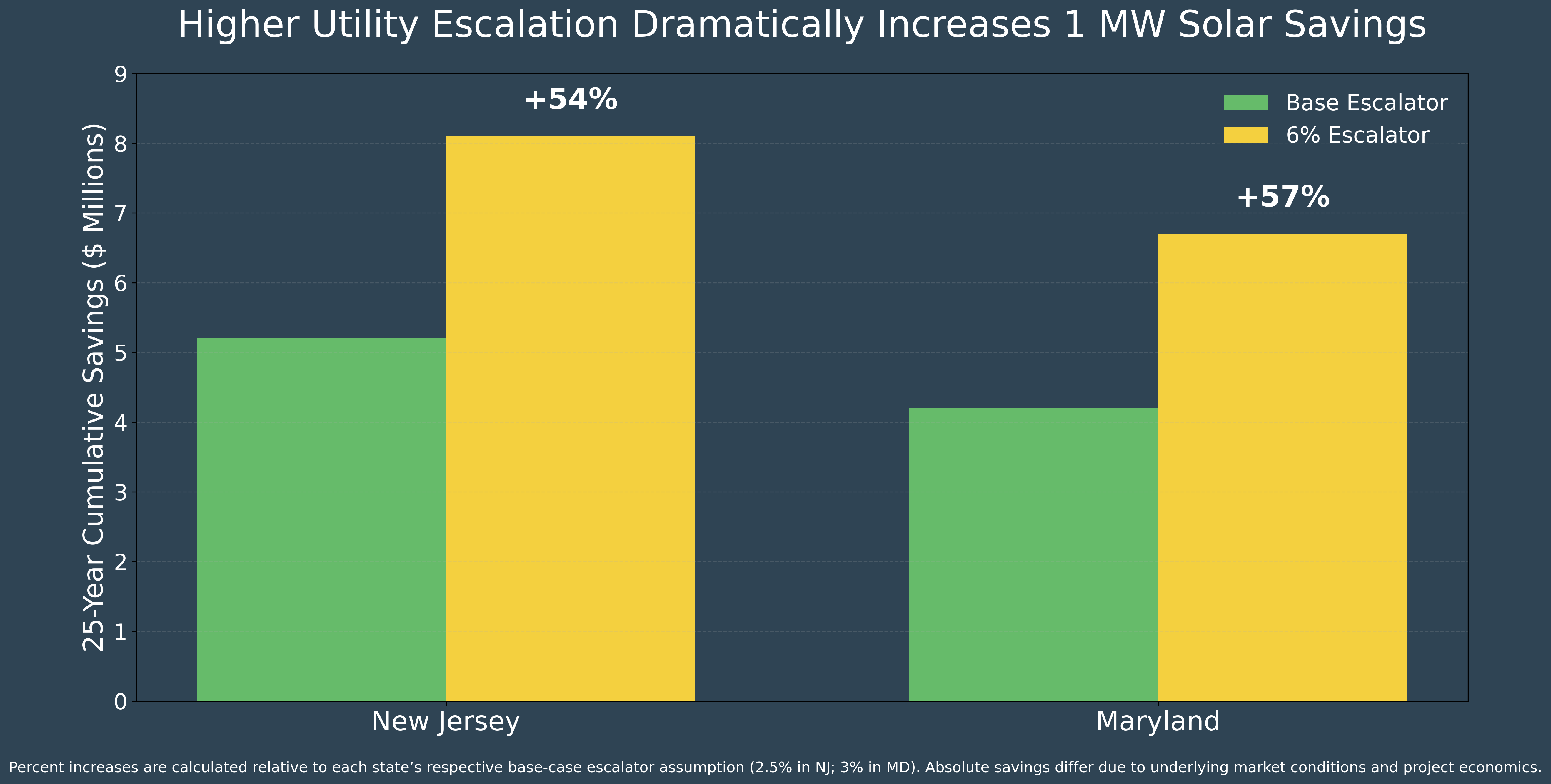

New Jersey continues to shine with the state community solar program. The most recent program capacity of 250 MW was released in June. More is expected later this year, but interconnection approval is crucial to acceptance, which can take months. The value of SRECs decreased slightly, but roof leases are still very lucrative.

In 2024, we evaluated New York (New York City and upstate New York) on commercial solar. We have downgraded the state from its initial A+ status to an A, reflecting the phaseout of key NYSERDA rebates and lower electricity rates in upstate New York.

Also in 2024, we tracked net metering rules that vary by state and utility. These rules determine how much a utility will pay for solar power sent to the grid. In Maine, recent legislative changes to net metering have been approved, but key implementation details remain in the hands of the Maine Public Utilities Commission (MPUC). With rulemaking still underway, solar developers are watching closely, as final decisions could reshape project economics across the state.

From a SolarKal perspective, Texas remains a highly deregulated and utility-dependent market, earning a C rating. A lack of centralized policy, unpredictable interconnection timelines, and extreme congestion risk make it a more challenging — and less consistent — opportunity. While we recognize the state for its vast solar market, most of the current activity is utility-scale solar.

A “D” rating does not signal impossibility. It just means that in 2025, the available incentives and regulatory climate are generally unfavorable for typical commercial solar projects. However, SolarKal evaluates each opportunity based on site- and client-specific goals. In certain cases, even low-rated states can yield viable returns, particularly with strong energy community eligibility or unique on-site usage profiles.

Tracking policy shifts across 50 states is complex but critical. Tackling that is our role. At SolarKal, we distill these policy insights into actionable guidance, helping commercial real estate owners make confident, well-timed decisions. This map is a tool to help guide those decisions and identify where momentum and margins are strongest. Curious what that means for your portfolio? It’s easy (and free) to connect with a SolarKal advisor and find out.

Connect With an Expert

See Your State's Solar Potential

See Your State's Solar Potential